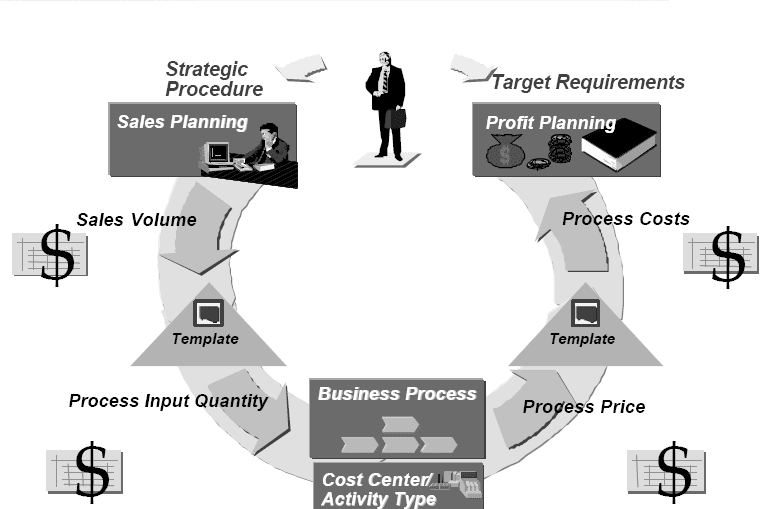

To fully integrate ABC into the corporate planning cycle, several new customizing activities should be performed.In order to identify ABC costs in the cost component view of product cost, new cost components for processes may be needed.New value fields may be needed for processes in CO-PA based on the new cost components.New value fields may be needed for processes in CO-PA, which are not product related.Activity Based Costing is also fully integrated into the corporate planning cycle when business processes are service oriented.The results of Sales Planning in CO-PA will also "back flush” (pull) a properly calculated amount of process quantities and finally of indirect resources (cost center/activity types) required to support the sales plan. To do this, business processes are assigned through the template directly to profitability segments (customers, divisions, distribution channels).

The back flushing of sales plan requirements results in the sales plan process quantity requirements being transferred to business process planning as scheduled quantities, where they may be compared to the original planned quantities.Once the plan and scheduled quantities have been reconciled the plan reconciliation program may be run which will replace the original plan quantities with the scheduled quantities. Alternatively, the scheduled quantities may selectively replace the original plan quantities through manual adjustments.Executing the process price calculation values the CO-PA plan. This means that the process costs will be transferred to Profitability Analysis (CO-PA).

Transfer of planned process consumption

The planning concept has been expanded to include process requirements. This achieves the same precision for indirect resources as has been available previously for direct resources.SOP supports both the high-level planning of complex planning hierarchies and the detailed planning of finished products.LTP is used to simulate the future stock and requirements for materials. It uses operative bills of material, routings, and work centers.Each of these two sales planning methods can transfer scheduled quantities to integrated ABC.The template is the tool that will transfer quantity requirements from either SOP or LTP to ABC.

Scheduled quantities can also be transferred from business processes, which are assigned to work centers used in routings.If this work center is assigned to a routing operation, the corresponding process is pulled. The standard values of the routing are used to calculate the process quantity based on PP formulas.Allocations to processes may be done using distribution, assessment and activity allocation. These techniques have long been available in R/3 and are not new to ABC.In addition to these methods, the template is a new tool for allocation. The new tool provides a more general capability than the other methods since it includes the use of formulas and functions. The use of templates results in a quantity and value flow.

Planning of Process Quantity Inputs

There are two approaches that may be used to plan process input quantities: activity allocation and template allocation.There are several activity allocation methods in R/3: direct, indirect and target = actual.The structured business process is a method of automating quantity allocations from both cost center/activity types and from other processes to a higher level process.Assessment or distribution methods may also be used to allocate costs from cost centers to processes but we then lose any ability to know the quantity of the indirect resources consumed by the processes.

Planning with Structured Processes

A structured process is described by a Template created in environment SBP.Planning starts with the output from the process, then calculates the required inputs to achieve the output. You can think of this as “ARP” - activity requirements planning, which is analogous to MRP - material requirements planning.In the structured template above, Process 1 is the top process in the resource allocation chain. For every output from Process 1, the template will automatically plan outputs from Process 21 and 22,based on the quantities found in Template 1. Then, resources will be allocated to Process 22 from the two cost center/activity types.Process 1 will pull a variable quantity of Process 22 based on Formula -2 and pull 20 fixed quantities of Process 22.

For every Process 22 output planned, Process 22 will pull 2 variable quantities from CC2/AT2, a fixed quantity from CC2/AT2 determined by “Formula -3” and 10 variable quantities of CC1/AT1. Note that cost center/activity types must be linked before they can be used in the structured process template. Linking is done whenever the combination of cost center/activity type is planned.The quantities which result from the structured process allocation are considered scheduled quantities.

Planning Statistical Key Figures

Statistical key figures can be planned on a business process in the same way as they can be planned on cost centers.Planned statistical key figures can serve as a tracing factor for an indirect activity allocation.They can also be used as the basis for resource allocation in the formula of a structured business process template.

Planning of Process Outputs

Output quantities of a process may be planned manually without identifying a specific cost object.Output quantities may also be planned in SOP / Long Range Planning which will integrate the process output with the sales and production plan.SOP/LTP will create “scheduled quantities” for the process. The plan reconciliation program will show you any discrepancies between the planned quantity and the scheduled quantity. It may also be used to automatically adjust the planned quantity to the scheduled quantity to eliminate any inconsistencies occurring from the planning effort.n Process outputs may also be planned with cost centers as receivers. An example might be the allocation of centralized administrative processes back to cost centers.When a Template is used for cost objects, the process type must be set to “manual entry manual allocation” (type 1).The planned process output is the basis for price determination of the process.

Plan Process Output Reconciliation

Before the plan is finalized, the planned relationships should be reconciled. This will show if any planned output quantities are unequal to scheduled input quantities.Any discrepancies in planned quantity may either be ignored, manually adjusted, or automatically adjusted through the reconciliation program.Each process carries its own unique price with fixed and variable components.

n The process pric e calculation is executed after planning the resource input to the process and the quantity output from the process.Only if one of the quantity planning methods have been used in providing indirect resources to the process will the system calculate a variable process price component.

The value of the variable quantity of resource inputs divided by the total quantity of the process output results in the variable process price. If fixed resource quantities have also been planned as process inputs, the value is divided by the total quantity of the process outputs to calculate the fixed process price.

Product Costing with Templates

Product cost planning includes the quantities and prices from the planned consumption of process quantities.The cost component view can be maintained in customizing to include processes in an aggregated view of process costs and quantities.In cost component customization, each component may be assigned as valuation relevant if the process costs should be included in inventory.The itemization view of the product cost estimate identifies process values with a code of "X." Overhead values calculated using a costing sheet are identified with a code of “G.”

Related Posts

No comments :

Post a Comment